The Flat Income Tax and the FairTax Consumption Tax

A Comparison of Federal Taxation Proposals

21

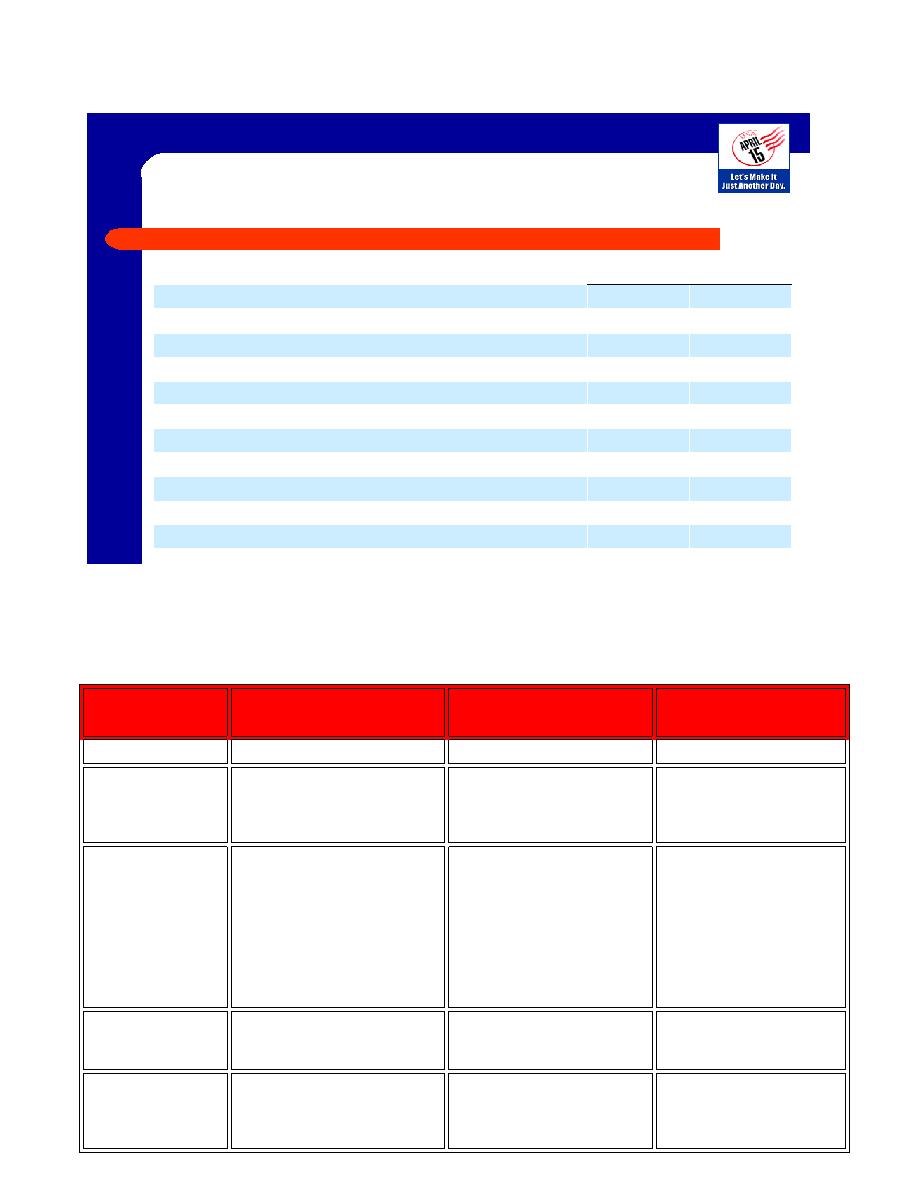

Flat Tax vs. Fair Tax

No

Yes

Taxes inherited and gifted wealth more fairly

No

Yes

Facilitates home ownership

No

Yes

Eliminates double taxation of business profits

No

Yes

Result in lower interest rates

No

Yes

Eliminates product tax build up in product cycle

No

Yes

Encourages investment

No

Yes

Encourages capital repatriation from tax havens

No

Yes

Stimulates exports

No

Yes

Simplifies business accounting and reporting

No

Yes

Eliminates $250 mil. Income tax industry

Yes

No

Is still an income tax

Flat Tax

Fair Tax

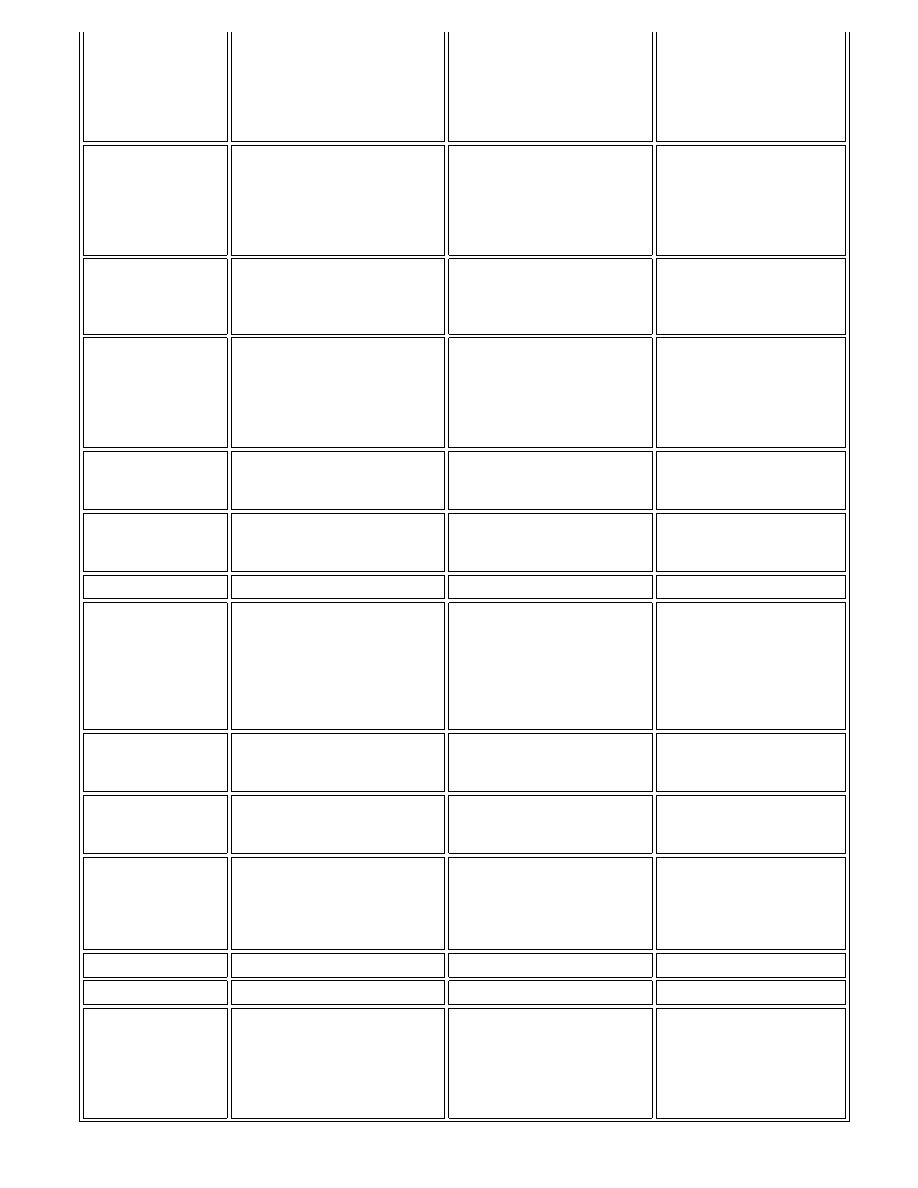

A Comparison of the FairTax SM, the Income Tax, and the Flat Tax

August 2001

FairTax, H.R. 25

Linder-AFFT

Federal Income Tax

Pre-2001 Law

Flat Tax, H.R. 1040

Armey

16th Amendment

Proposes repeal.

No change.

No change.

Complexity

Individuals do not file.

Businesses need only to deal

with sales tax returns.

Very complex; 20,000 pages

of regulations; I.R.S. incorrect

over half of the time.

Withholding continues.

Individuals and businesses

must still track income and

file income tax forms.

Congressional

Action

23% Linder/Peterson FairTax

Act of 2001 (H.R. 2525).

Employees receive 100% of

pay. Social Security and

Medicare funded from

consumption tax revenue, not

your paycheck.

(H.J.Res45) - Will repeal the

16th Amendment.

Used by lobbyists and the

wealthy for tax-breaks and

loopholes. Used by

bureaucrats for social

engineering.

Rep. Armey's H.R. 1040

has some problems, but is

far superior to current law.

It would impose a 17% Flat

Tax on income.

Cost of Filing

No personal forms are filed.

Significant cost savings.

$225 billion in annual

compliance costs

Significant simplification

costs are somewhat

reduced.

Economy

Un-taxes wages, savings, and

investment. Increases

productivity. Produces

significant economic growth.

Taxes savings, labor,

investment, and productivity

multiple times.

Imposes a tax burden

some of which is still

hidden in the price of

goods and services.

Equality

Taxpayers pay the same rate

and control their liability. Tax

paid depends on life style. All

taxes are rebated on spending

up to the poverty level.

The current tax code violates

the principle of equality.

Special rates for special

circumstances violate the

original Constitution and are

unfair.

The flat tax is an

improvement over the

current income tax, but it is

still open to manipulation

by special interests.

Foreign

Companies

Foreign companies are forced

to compete on even terms with

U.S. companies for the first

time in over 80 years.

Current tax code places

unfair tax burden on U.S.

exports and fails to neutralize

tax advantages for imports.

A flat tax taxes exported

goods and does not tax

foreign imports to the U.S.,

creating unfair competition

for U.S. manufacturers and

businesses.

Government

Intrusion

As the Founding Fathers

intended, the FairTax does not

directly tax individuals.

Current tax code requires

massive files, dossiers,

audits, and collection

activities.

A flat tax still requires

personal files, dossiers,

audits, and collection

activities.

History

45 states now use a retail

sales tax.

The 1913 income tax has

evolved into an antiquated,

unenforceable morass, with

annual tax returns long

enough to circle Earth 28

times.

A flat tax just won't stay

flat. Starting out nearly flat

in 1913, the income tax

grew out of control with top

rates over 90% until the

Kennedy administration.

Interest Rates

Reduces rates by an estimated

25-35 percent. Savings and

investment increase.

Pushes rates up. Biased

against savings and

investment.

Reduces rates 25-35

percent. Neutral toward

savings and investment.

Investment

Increases investment by U.S.

citizens, attracts foreign

investment.

Biased against savings and

investment.

Neutral toward savings and

investment.

IRS

Abolished.

Retained.

Retained with reduced role.

Jobs

Makes U.S. manufacturers

more competitive against

overseas companies.

Escalates creation of jobs by

attracting foreign investment

and reducing tax bias against

savings and investment.

Hurts U.S. companies and

decreases available jobs.

Payroll tax a direct tax on

labor.

Positive impact on jobs.

Does not repeal payroll tax

on jobs.

Man-hours

required for

compliance

Zero hours for individuals.

Greatly reduced hours for

businesses.

Over 5.4 billion hours per

year.

Reduced.

Non-filers

Reduced tax rates and fewer

filers will increase compliance.

High tax rates, unfairness

and high complexity harm

compliance

Reduced tax rates and

improved simplicity will

improve compliance.

Personal and

Corporate Income

Taxes & FICA

Social Security

Taxes

Both are abolished. FICA

Social Security payroll

withholding eliminated also,

and funded within the sales tax

revenues at today levels.

Retained. Both employee and

employer will still pay 7.65%

each into Social Security

Retained in a different

form. Both employee and

employer will still pay

7.65% each into Social

Security.

Productivity

Increases.

Inhibits productivity.

Increases.

Savings

Increases savings.

Decreases savings.

Increases savings.

Visibility

The FairTax is highly visible

and easy to understand. No

tax is withheld from paychecks.

The current tax code is

hidden, embedded in prices,

complex, and

incomprehensible. Taxes are

withheld from paychecks.

The business component

of the flat tax and payroll

taxes are hidden and would

be embedded in prices.

Taxes are withheld from

paychecks.

Testimony by the Arthur Hall, Tax Foundation and before the House Ways and Means Committee, 1998

The Flat Income Tax and the FairTax (HR 25) Consumption Tax

A Comparison of Federal Taxation Proposals

Tax Rate Comparison An Income tax is an Inclusive Tax a Sales Tax is an Exclusive Tax

Flat Tax System - 24.65% (inclusive including FICA social security tax) = 32.5% (exclusive rate )

=17% (inclusive withholding income tax rate) + 7.65% separate inclusive FICA Social Security tax rate

= 24.65% total inclusive tax rate (converts to 32.5% exclusive rate) under the current Flat Tax proposal

ALL personal income and business profits are taxed first, which translate to a tax on ALL consumption and

savings (made with after tax dollars), thus translating to a tax on all new goods, used goods, services, savings,

investment, education, charity, estate and gift giving, busines to business purchases and tax on some State tax

payments (tax on tax). Mortgage interest only and charity giving over a certain level is not taxed through a refund

deduction, and there is a standard deduction (tax free income) for dependents. Additionally employers will also

pay 7.65% in FICA for each worker, reducing the salaries for everyone by a comparable amount. Self Emp. FICA

is 15.3% inclusive. Filing of multiple forms is done at the end of the year to receive overpayment or return of taxes

paid on dependents, mortgage interest and charity donations above certain levels.

FairTax System - 23% (inclusive rate includes FICA) = 30% sales tax (exclusive sales rate includes FICA)

on consumption of NEW Goods & Services ONLY at the point of end use retail only.

No tax on initial spending up to the HHS poverty level for ALL households determined by number of dependents

only. Paid for with before tax dollars, there is no tax on any used items, no tax on any and all savings or

investment, no tax on any business profits, no tax on any education expenses, no tax on any existing mortgage or

other loan payments both interest and principal, no tax on any charitable giving, no tax on any estate and gift

giving, No tax on ALL State and Local taxes paid. No tax on business to business transactions. No filing of any

kind is necessary at the end of the year to receive a tax refund on any of the tax exempt items, as no tax was

actually paid initially on these items when the purchase or saving, or giving took place. FICA social security is paid

through the sales tax receipts funding social security benefits for you at today's levels. You pay the appropriate tax

exactly, when you spend, and in your time, based on your personal choices.

Inclusive and Exclusive Tax Rate Comparisons Apples to Apples

All tax systems should be quoted in the same form of tax rate structure and include both General Fund & FICA.

Inclusive tax rate = tax rate as a percentage of the total dollar paid out or earned = the way current Income Tax ,

FICA payroll tax and Flat Tax rates are quoted.

24.65% inclusive Flat Tax plan including FICA payroll tax (17% Flat Tax + 7.65% FICA)

of every $100 of earned income from all sources - $24.65 goes to the tax man and $75.35 you can keep

23% inclusive FairTax Plan including Social Security funding within the sales tax rate itself

of every $100 spent in the market place on new goods and services - $23 goes to the tax man and $77 is

your buying power

Exclusive tax rate = the tax payment as a percentage of income left or price of the item being purchased

32.7% exclusive Flat Tax including FICA = (24.4% exclusive Flat tax + 8.3% exclusive FICA tax)

means if you have $75.35 left in your pocket after taxes, you actually had to earn 32.5% more ($24.65) or

$100 total in income to begin with

30% exclusive FairTax sales tax rate at the register (which includes paying for Social Security)

means if you want to purchase an item for $77 you will have to pay an additional 30% ($23) in sales tax

or $100 total at the register for that item.

Notice in both inclusive and exclusive terms, the dollars paid in tax, and the dollars left to spend for Flat Tax are

the same ($24.65 in tax and $75.35 left to spend) and for FairTax are the same ($23.00 in tax and $77.00 left to

spend). Inclusive and exclusive while they apear to be different percentage rates, actual produce the same

results. It's a matter of 12 inches = 1 foot....you can't just look at the number to compare you have to look at the

label too.

Social Security Funding

Flat Tax Social Security FICA payroll taxes remain in place designated as a 7.65% inclusive tax on wages for

each worker up to first $92,000 earned. Employers will continue to match this with 7.65% on wages paid, making

the total tax burden for FICA under Flat Tax = 15.3% (inclusive) per wage earner - Self employed workers will pay

15.3% on their own earnings for FICA.

FairTax Social Security is fully funded within the 30% (excusive) Sales tax collected at consumption on new

goods and services at end use retail. The current 7.65% FICA payroll withholding for each employee and the

7.65% employer matching payment will be eliminated completely for all wage earners and their employers. Self-

employed business owners will also have their 15.3% FICA tax payment eliminated. 1/3 of every dollar collected

through the sales tax is designated within HR 25 to be used as social security revenues, and will fund the Social

Security system at today's levels, without a change to any benefits, while all savings and investment will be done

at any level totally tax free. This is the ultimate in Social Security privatization.

Tax Payer Base

Flat Tax While there will be a small increase in the number of working citizens that will pay into the Flat income

tax system, due to the elimination of many deductions and loopholes, there will still be those that receive

Government benefits of all types, that will escape paying into the Federal Flat Tax system. Examples are those

working within the underground economy; those 20 million that are not here legally and are not reporting wage

income; those who visit the U.S.A. as tourists, using our benefits of roads and protection, but not paying anything

toward those benefits.

FairTax Everybody pays into the system at point of consumption of new goods and services. Illegal citizens,

tourists, those spending dollars earned "under the table" or through illegal means, currently not paying income tax,

will all pay the sales tax when they consume, thus broadening the base of those paying into the system. This

broader base of taxpayers will also be paying into the Social Security system, as it is also funded by the sales tax.

A broader base, means a lower tax rate for all. The tax free spending exemption up to the poverty level that will be

given to everyone in the form of a rebate monthly, will make the poor and lower income tax free. However, they

will still be part of the sales tax system, and will pay their fair share of consumption taxes on new goods and

services as their income goes up beyond the poverty level, like everyone else.

Both the Flat Tax and the Consumption Tax Reduce Marginal Tax Rates Dramatically, Although a

Consumption Tax Will Reduce Marginal Tax Rates More Than a Flat Tax

Flat tax supporters often emphasize, correctly, that marginal tax rates, rather than average or effective, are the

most economically relevant tax rates. It is marginal tax rates that affects an individual's decision about what to do.

A consumption tax can be viewed as imposing a zero marginal tax rate on labor and capital income, if the

economic incidence of the tax is on consumers. Alternatively, one can view the incidence of the consumption tax

on the factors of production (labor and capital). The comparison below is based on the view that the consumption

tax is incident on the factors of production.

The flat tax bill would reduce the top marginal income tax rate to 17%. This rate, however, is not revenue neutral.

The flat tax is revenue neutral at about a 21-22% rate, not taking into account the impact of the plan on economic

growth. In the real world, the flat tax would cause economic growth that would increase the tax base, perhaps

reducing the revenue neutral tax rate to 20% (within a few years). The flat tax would not affect the employer or

employee Social Security or Medicare payroll tax. Those that have earnings below the Social Security wage base

($72,600 per worker in 1999) would, therefore, face a marginal tax rate of 32.3%. Taxpayers over the Social

Security wage base would face a marginal tax rate of 19.9% on wage income and 17% on capital income. These

figures are about 3-5% points higher in a revenue neutral flat tax.

Under a federal consumption tax, the poor would experience negative effective tax rates because of the universal

rebate. They would pay no tax up to the poverty level. Middle-income and affluent taxpayers would pay 23% at the

margin. It should be noted that since taxes have crept up over the past several years, the revenue neutral tax rate,

without taking into account economic growth, is approaching 25%. Once the FairTax-induced economic growth is

taken into account, 23% would probably raise as much revenue as the current system.

Thus, middle-income taxpayers would pay a much lower marginal tax rate under the consumption tax than under

the flat tax. This is because the FairTax replaces payroll taxes as well as the income tax. Affluent taxpayers would

pay comparable marginal tax rates under the consumption tax and the flat tax. These differences are summarized

in the table below.

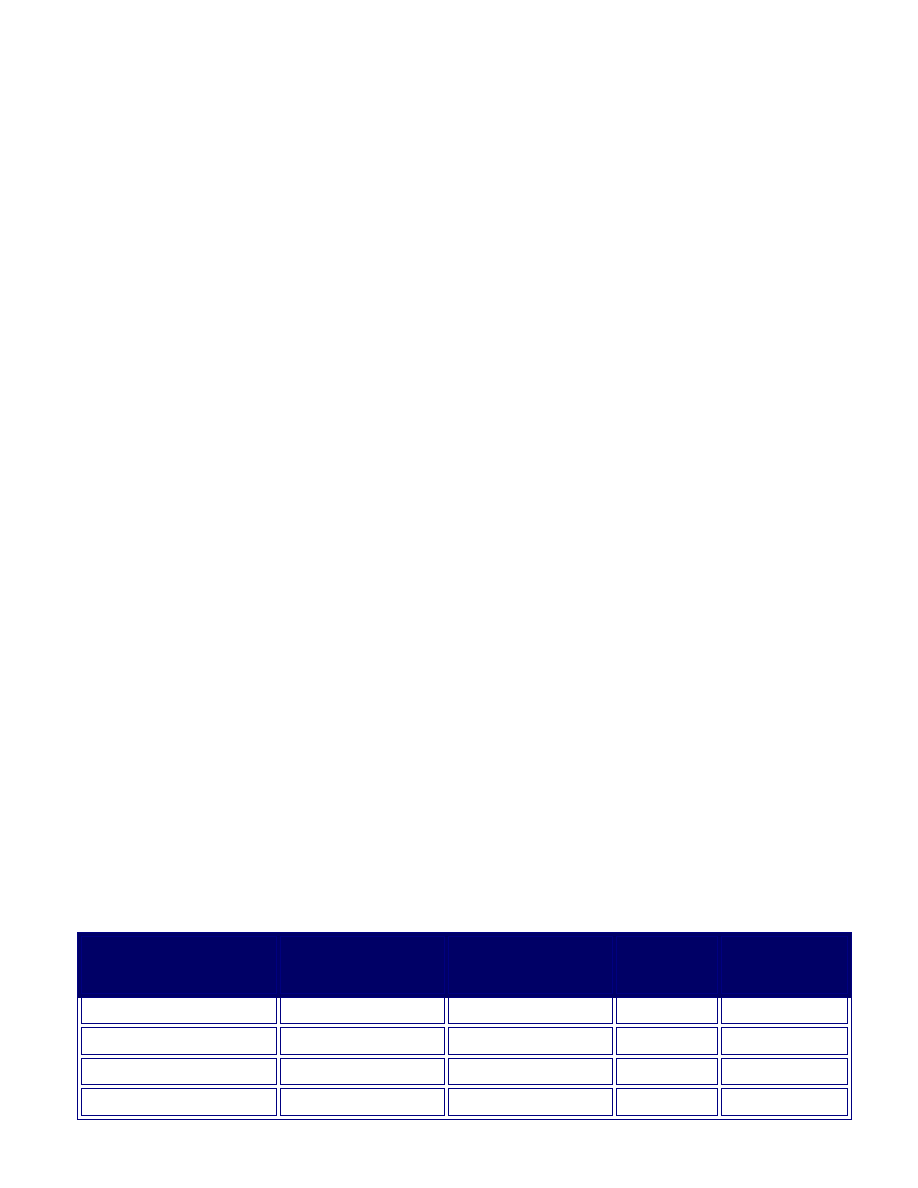

Comparative Marginal Tax Rates

Type of Person

Armey-Shelby

Revenue Neutral Flat

Tax (+3)

FairTax

(Consumptio

n Tax)

Difference

Poor

15.3

15.3

0

-15.3

Middle Class

32.3

35.3

23

-12.3

Affluent (capital)

17

20

23

+ 3.0

Affluent (salary)

19.9

22.9

23

+ 0.1

The FairTax generally has a more positive impact on marginal tax rates than does the flat tax.

Both the Flat Tax and the Federal Consumption Tax Are Neutral Toward Savings and Investment

The flat tax and the consumption tax both remove the income tax bias against savings and investment. The flat tax

accomplishes this result by expensing capital costs and exempting the return on savings. The consumption tax

accomplishes this same result by only taxing final consumption sales. Each would result in higher levels of savings

and investment, higher rates of capital formation, higher productivity, and higher real incomes.

Both the Flat Tax and the Federal Consumption Tax Promote Economic Growth, but the

Consumption Tax Will Be More Pro-Growth

Since it will have a better impact on marginal tax rates and the arguably equivalent tax on capital investment, the

consumption tax will have a more positive impact on economic growth. Moreover, because U.S. and foreign

producers for overseas markets can produce goods and services tax free under a consumption tax, but not under

a flat tax, the consumption tax will have a relatively more positive impact on economic activity in the U.S.

The Consumption Tax Does a Better Job of Eliminating Work Disincentives for the Poor

Since the Consumption Tax plan removes the payroll tax while the flat tax keeps the payroll tax (and repeals the

earned income tax credit), the FairTax will make it easier for the working poor to climb out of the dependency trap.

In contrast, the working poor will continue to pay the 15.3% payroll tax on their first dollar earned under the flat tax.

Under the FairTax, payroll taxes are repealed and a rebate of the consumption tax on expenditures up to the

poverty level is provided. Thus, the marginal tax rate the poor will face is zero, and therefore, lower under the

consumption tax than under the flat tax.

The flat tax is biased against workers because only those earning wages pay the tax. Those that earn income from

capital gains (such as those with personal wealth) can avoid paying their fair share of taxes. This makes it less

palatable to the American public.

A Flat Tax is Easy to Convert Back Into an Income Tax

Under the flat tax, the I.R.S. continues to exist. They will administer a system that is not structurally different from

the income tax. All individuals and businesses will file tax returns.

With five simple changes, the flat tax can be converted into a graduated income tax. Step one is to depreciate

rather than expense capital costs. Step two is to make interest expenses deductible and interest income taxable.

Step three is to tax capital income (such as dividends and rent) and capital gains. Step four is not to allow

inventory purchases to be deducted until the inventory is sold. A fifth step is to impose graduated rates, which

would complete the transition back to a graduated income tax.

After a consumption tax is enacted, it will be virtually impossible to go back to an income tax. The I.R.S. will no

longer exist because the states will, for the most part, be administering the tax system. The entire income tax

apparatus will have disappeared, and the expertise in administering this present Byzantine system will be

dispersed. People will have gotten used to not filing returns and will not want to go back to the old system. People

will have gotten use to keeping what they earn and will not want to go back to withholding.

Although it is also quite possible to apply graduated rates under a flat tax, it is not possible to impose graduated

tax rates on individuals or businesses under the FairTax because the consumption tax is an indirect tax imposed

on goods and services.

A Consumption Tax Actually Gets Rid of the I.R.S.

In general, states would administer the federal consumption tax because they already have the expertise. States

would not be required to administer the tax; however, in most cases, they would choose to do so. FI.R.S.t, they will

be provided with a generous administration fee to administer the federal tax. Since 45 states already administer

sales tax systems, the incremental costs of implementation of the FairTax will be low (particularly if the state

conforms its tax base to the federal tax base). Second, for the fI.R.S.t time, states will be able to tax direct mail

sales originating in their respective states under this integrated system. This will broaden the state's tax base and

put all retailers on an equal footing. Third, states will know that if they do not administer the tax, the federal

government will do so. Given that choice, they will want to do it themselves for reasons of control and professional

pride.

Compliance Costs Will Be Lower Under a Consumption Tax Than Under a Flat Tax

A flat tax would simplify the tax code considerably. However many of the complexities of current tax law would

remain. For example, tremendous pressure, would be placed on intercompany pricing rules since offshore income

is exempt from tax. Manipulating the prices at which goods change hands between a U.S. company and its foreign

affiliate could zero out the U.S. source income under a flat tax. Under a flat tax, the cost of employee benefits,

interest, insurance, and other costs must be segregated since they are not deductible. The current complex

pension system stays largely intact. Under a consumption tax, the question is simply how much did a firm sell to

consumers.

The Flat Tax May Require Only a Postcard for Wage Earners, but the Consumption Tax Requires

No Tax Return At All

Flat tax proponents are proud that their individual tax form will fit on a postcard. So, of course, could today's 1040

EZ. Under a consumption tax, individuals who are not in business for themselves will file no return. No return is

preferable to a postcard.

A Federal Consumption Tax Is Much Easier for the Public to Understand Than the Flat Tax

A federal consumption tax is something that is easily explained and understood by the public. Flat tax proponents

have had difficulty explaining it to the American people, notwithstanding large budgets, Mr. Forbes's Presidential

campaign, the efforts of Majority Leader Armey, the Heritage Foundation, Citizens for a Sound Economy, and

others.

Perhaps the most obvious problem with explaining the flat tax is the issue of capital income. Again and again, it

has been argued that the flat tax does not tax "coupon clippers." This argument is made in response to the

allegation that rich people can live well and tax free on interest and dividends and pay no tax while the working

stiff has to pay tax. Although this allegation is false because the tax on that income is effectively withheld at the

business level, flat tax proponents have failed in their efforts to get their message across.

The Consumption Tax Is More Visible

Under the flat tax, much of the tax burden is hidden in the business tax. Will recipients of dividend and interest

payments actually understand that a withholding tax has been imposed by denying a deduction to the business

making the payment? Will recipients of employer-provided fringe benefits understand that a withholding tax has

been imposed by denying the employer a deduction for the benefits? Will the non-deductibility of employer taxes

be understood as tax increases? In all cases, it is highly doubtful. Thus, hundreds of billions of dollars in taxes are

hidden under a flat tax.

There are those who believe that hiding taxes from the American people is a good thing, because if the people

actually understood the true level of the tax burden, they wouldn't stand for it. The consumption tax, however,

works on the principle that taxes should be visible and fairly convey the true cost of government. The consumption

tax will by law be shown on every retail purchase sales receipt, and this provision will be mandatory.

The Consumption Tax Is Not a VAT and Will Not Turn Into One; the Flat Tax Is a VAT

Flat tax supporters who are also consumption tax opponents often argue that a consumption tax would turn into a

value-added tax (VAT). VAT's are usually hidden taxes, collected at each stage of production.

The consumption tax is not a VAT since the consumption tax is collected at the retail level, and no tax is imposed

on intermediate sales.

The flat tax is a VAT. None other than the father of the flat tax, Robert Hall of Stanford University (along with Alvin

Rabushka), in his 1995 Ways and Means Committee testimony said, "The Hall-Rabushka flat tax is a value-added

tax." Thus the flat taxers are effectively attacking their own proposal when they attack a VAT. Most, however, do

not understand their own proposal well enough to understand this.

The flat tax is not an income tax because its tax base is not income. At the business level, value added by capital

is taxed by the flat tax. At the personal level, labor value added is taxed. The business tax burden under the flat

tax is much higher than under current law. Interest expense, most insurance expenses, taxes (including payroll

taxes), rent, and other expenses are not deductible under the flat tax. The aim of the flat tax is not to measure net

income, but value added.

The flat tax is identical to the USA Tax business tax, an acknowledged subtraction method VAT, except in two

respects. First, the flat tax taxes exports and exempts imports from tax. This makes it an origination principle VAT

instead of the usual destination principle VAT. The other difference is that business can deduct wages in the flat

tax, but not in normal VAT's. The flat tax individual tax, however, is a wage tax. Thus, the flat tax taxes wages just

like a normal VAT. However, because it taxes wages at the individual level, the flat tax taxes most government

value-added, while normal VAT's do not.

Tax Evasion Under Both Systems Will Be Comparable

Under a consumption tax, the number of persons that the tax administration authorities must focus on is reduced

by 80% or more. Only businesses are in the tax system. Dramatically lower marginal tax rates -- lower for most

than the flat tax -- will reduce the marginal benefit to cheat. If enforcement and associated penalties remain

comparable, and the marginal benefit to cheating falls, evasion should decline. The overall legitimacy of the

system will improve, and non-compliance generated by frustration or hostility will decline. Individuals who are not

in business, and non-retail businesses will be unable to cheat on their taxes, since they will not be in the system.

Retailers would benefit equally from cheating under the flat tax and the consumption tax (assuming the rate were

the same). Let's take a bar owner that pockets $1,000 per week and fails to report his sales either to the income

tax, flat tax, or consumption tax authorities. In the world of either the income tax or the flat tax, that pocketed

$1,000 will reduce the owner's gross revenues, and therefore, his profits by $1,000 per week. He will, of course,

continue to report all of his expenses. He will retain the documentation for the wages he paid and the liquor he

bought. The government will lose revenue equal to the tax rate times the $1,000 per week. In a consumption tax

world, the government will loose revenue equal to the consumption tax rate times the $1,000 per week. In both

cases, the loss to the government is the same.

The Transition Is Easier Under a Consumption Tax Than Under a Flat Tax

Under the flat tax, the tax liability of the business community increases dramatically, by hundreds of billions of

dollars per year. All capital value added is taxed at the business level. Only wages are taxed at the individual level.

About $5 trillion worth of future deductions (remaining basis), relating to inventory acquisitions, depreciation on

capital investment made under the income tax, and so on, exist under the income tax. Since the return on these

assets would be in the flat tax taxable base, failure to allow these deductions would amount to a confiscation of

nearly one-fifth of existing wealth. The business community, large and small, will not let the flat tax pass without

transition rules.

For example, under the Armey-Shelby flat tax if you bought a building for $1 million dollars the day before the bill

went into effect and sold it for $1 million the day after the bill went into effect, you would have taxable income of $1

million (even though you have no profit) since the bill assumes that you have expensed the building. In the real

world, the taxpayer's income tax basis in that building is going to have to be deductible. The revenue from this kind

of expropriation is presently counted in flat tax revenue estimates.

Allowing these deductions, however, would increase the revenue neutral tax rate in the flat tax considerably.

Alternatively, the transition could be funded by a complex series of taxes on various windfall gains accruing to

certain businesses or taxpayers.

Under the consumption tax, corporations and other businesses and investors pay no tax on their income.

Accordingly, it is doubtful that any transition "relief" is appropriate. The future income of their assets will be tax free.

Transition rules are only appropriate with respect to inventory held on the date of the changeover, since those

inventory costs would not have been deducted in the income tax and the sale of the inventory will be taxed. Rules

need to be provided to ensure that the CPI used to index benefit payments includes the consumption tax to protect

against any consumption tax induced price increases (although it is not clear there will be any, since repealed

income and payroll taxes account for 20-25% of the price of goods and services, according to Harvard economics

department Chairman Dale Jorgenson). That's about it. The transition is a much simpler problem under a

consumption tax.